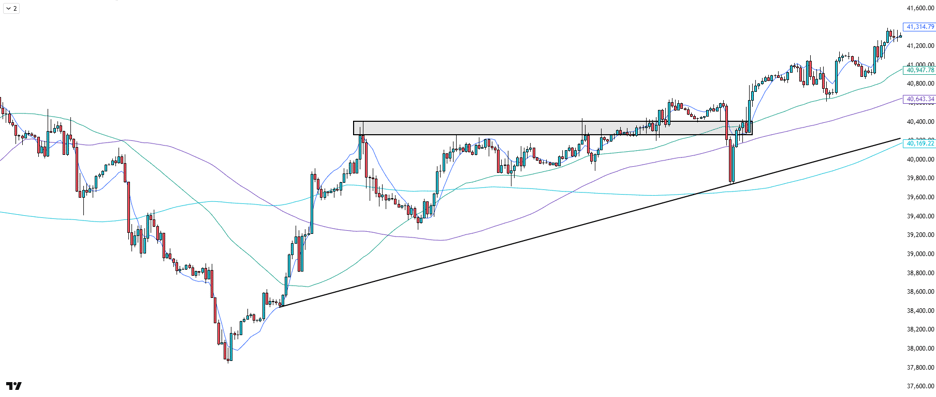

The final week of April and start of May 2025 saw the Dow Jones Industrial Average extend its winning streak, closing higher in all five sessions and notching its ninth consecutive daily gain by Friday, May 2nd. This marks the index’s longest such run since 2004—driven by improving macro sentiment, resilient earnings, and a decisive technical breakout that captured the attention of institutional traders.

The week began with the Dow consolidating just beneath a clearly defined supply zone between 40,800 and 41,000, a level that had capped price for much of the prior week. Early sessions saw muted action, but the price held above key short-term moving averages—signaling healthy underlying demand. Notably, the index respected a rising trendline that had been in place since the April 19th bottom near 38,000. This trendline, tested several times through the week, served as a critical reference point for bulls.

By Wednesday, a clear catalyst emerged in the form of easing geopolitical rhetoric and a wave of corporate earnings surprises, particularly from industrials and large-cap tech. Price surged through resistance, retesting the 40,800–41,000 level from above—a textbook breakout-retest-confirmation pattern. The reaction was clean, with no significant wick rejection or volume anomalies, suggesting the move was driven by real order flow rather than short-covering alone.

By Friday’s close, the Dow had made a clean push toward 41,314, its highest level in over two months. The 20-period exponential moving average sloped sharply upward, while the 200-period moving average flattened out—often an early signal that a trend is transitioning from neutral to bullish. The overall structure, marked by higher lows, higher highs, and rising moving average confluence, offered clear validation to those positioned long.

Market breadth, while not euphoric, broadened notably, with financials, industrials, and select tech components showing follow-through. Meanwhile, Apple’s earnings miss on Thursday caused a momentary dip, but broader index strength absorbed the shock with little impact—further reflecting improving resilience.

From a macro perspective, the week’s bullish tone was underpinned by a strong jobs report and subtle softening in US-China trade tensions. The 10-year Treasury yield drifted modestly higher to 4.3%, but risk appetite remained intact. Traders appeared willing to stomach higher rates in exchange for earnings visibility and geopolitical stability.

As the Dow heads into May, the key question is whether this rally has legs. Technically, so long as price holds above the 40,800–41,000 breakout zone, the path of least resistance remains to the upside. Friday’s close near session highs—without a late-day fade—suggests that institutional flows remain supportive. For now, the bulls are in control.